K11 Loses, SKP Thrives: Who’s Winning China’s Luxury Mall Battle? | Analysis

While Hong Kong malls still lead in the numbers, Mainland malls are catching up in sales.

Hong Kong-based developer New World Development recently announced a loss of nearly HK$20 billion for fiscal year 2024, with former CEO Adrian Cheng stepping down. Cheng is also the CEO of K11, a high-end shopping mall chain in Hong Kong. K11 operates major malls like K11 Musea, K11 Art Mall, and 11 Skies in Hong Kong and has expanded to five mainland Chinese cities, with plans to reach 10 cities by 2026.

Hong Kong vs. Mainland China Powerhouses

In China’s luxury mall landscape, there are two main players:

the Hong Kong-based group, including K11 (New World Development), Plaza 66 (Hang Lung Properties), IFS (The Wharf Holdings), IFC (Sun Hung Kai), and Taikoo Li (Swire Properties);

and the mainland-backed players such as SKP, MixC, Deji, and Wushang.

In terms of numbers, Hong Kong-backed malls still lead. Hang Lung’s Plaza 66 has over nine locations in mainland China, IFS has five, and Taikoo Li has four. However, mainland malls like SKP, MixC, and Hangzhou Tower are catching up in sales.

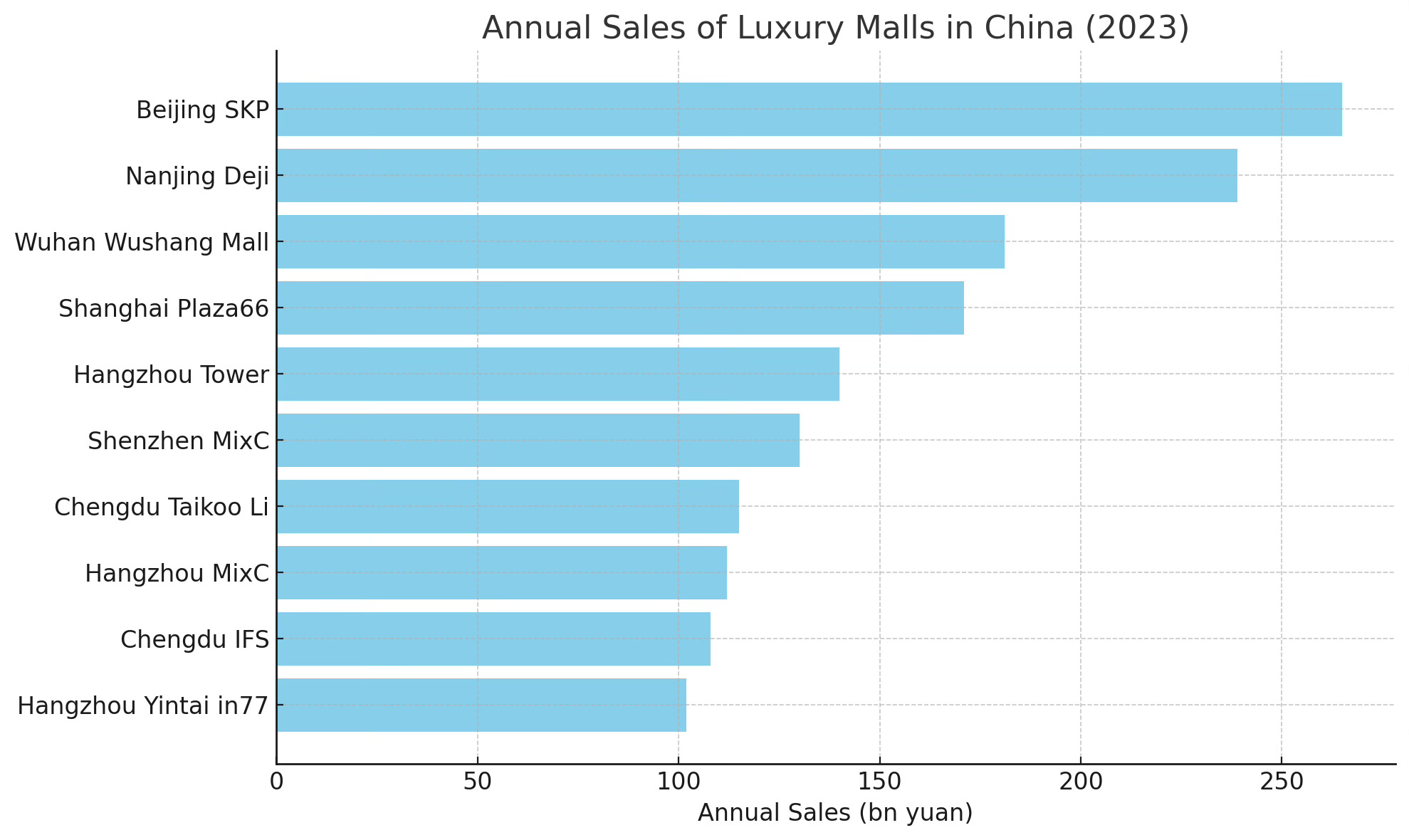

Last year, Beijing SKP retained its title as the top-selling mall in China, with sales reaching 26.5 billion RMB, continuing a five-year streak. Since surpassing Hangzhou Tower in 2011, SKP has consistently held the top spot for single-store sales in China. Other malls, like Nanjing Deji Plaza, also continue to perform well, with 2023 sales reaching 23.9 billion RMB, a 13.8% year-on-year increase. Beijing's China World Mall also surpassed 20 billion RMB in sales in 2022.

In the top 10 luxury malls in China by sales for 2023, seven are mainland shopping malls. Among Hong Kong-backed malls, only Shanghai Plaza 66, Chengdu Taikoo Li, and Chengdu IFS made the list. None of the K11 malls reached 10 billion RMB in annual sales.

Price War, Government Backing, VIP Services: How Mainland Luxury Malls Outperform

Mainland Chinese luxury malls have become formidable competitors to their Hong Kong counterparts, and here are key factors explaining why they are winning the battle.

Government Support

Local government backing plays a decisive role in the success of mainland luxury malls. For example, Wuhan Wushang Mall and Hangzhou Tower are owned by state-run companies, Wushang Group and Hangzhou Jiebai Group respectively. These malls enjoy local protection policies, securing the best locations and controlling significant market share before foreign or Hong Kong-invested malls can enter the scene.Aggressive Price Wars

Mainland malls are able to engage in aggressive price wars thanks to their strong capital backing. A prime example occurred when SKP entered Wuhan, sparking a luxury price war. Wuhan Wushang Mall offered the steepest discounts, leveraging its financial strength to attract more consumers and defend its market position.Consumer-Centric Strategy

Mainland luxury malls have a deeper understanding of Chinese consumers compared to Hong Kong-invested malls, which tend to stick to a more traditional approach. For instance, SKP uses a buyer-driven model to carefully curate products, offering exclusive items and requiring uniform signage for luxury stores. SKP also leverages a VIP membership system, encouraging repeat business and offering personalized services that keep loyal customers coming back.Expansion and Innovation

Mainland malls, particularly those owned by conglomerates like China Resources (which operates MixC malls), are rapidly expanding and introducing innovative mall formats. For example, MixC malls are developed as mixed-use complexes that combine retail with entertainment and cultural spaces, providing a unique shopping experience. This flexibility and adaptability allow them to appeal to a broader range of consumers.

While Hong Kong malls like Swire Properties' Taikoo Li pioneered the "block street" format—seen in successful developments like Sanlitun and Chengdu Taikoo Li—mainland malls are proving more agile in responding to shifting market trends and consumer preferences. Their localized strategies, strong financial backing, and government support continue to set them apart in the increasingly competitive luxury retail landscape.